Page 350 - Microsoft Word - 00 IWB ACCA F7.docx

P. 350

Chapter 24

Example 1 cont.

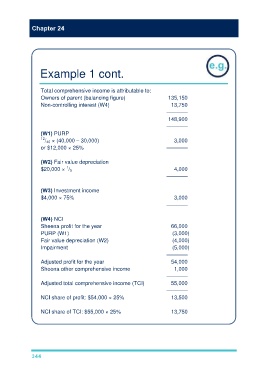

Total comprehensive income is attributable to:

Owners of parent (balancing figure) 135,150

Non-controlling interest (W4) 13,750

–––––––

148,900

–––––––

(W1) PURP

12 / 40 × (40,000 – 30,000) 3,000

or $12,000 × 25% –––––––

(W2) Fair value depreciation

1

$20,000 × / 5 4,000

–––––––

(W3) Investment income

$4,000 × 75% 3,000

–––––––

(W4) NCI

Sheena profit for the year 66,000

PURP (W1) (3,000)

Fair value depreciation (W2) (4,000)

Impairment (5,000)

–––––––

Adjusted profit for the year 54,000

Sheena other comprehensive income 1,000

–––––––

Adjusted total comprehensive income (TCI) 55,000

–––––––

NCI share of profit: $54,000 × 25% 13,500

NCI share of TCI: $55,000 × 25% 13,750

344