Page 356 - Microsoft Word - 00 IWB ACCA F7.docx

P. 356

Chapter 24

Chapter 20

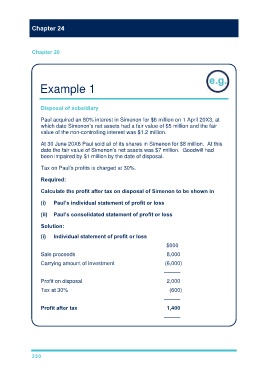

Example 1

Disposal of subsidiary

Paul acquired an 80% interest in Simenon for $6 million on 1 April 20X3, at

which date Simenon’s net assets had a fair value of $5 million and the fair

value of the non-controlling interest was $1.2 million.

At 30 June 20X6 Paul sold all of its shares in Simenon for $8 million. At this

date the fair value of Simenon’s net assets was $7 million. Goodwill had

been impaired by $1 million by the date of disposal.

Tax on Paul’s profits is charged at 30%.

Required:

Calculate the profit after tax on disposal of Simenon to be shown in

(i) Paul’s individual statement of profit or loss

(ii) Paul’s consolidated statement of profit or loss

Solution:

statement of profit or loss

$000

Sale proceeds 8,000

Carrying amount of investment (6,000)

———

Profit on disposal 2,000

Tax at 30% (600)

———

Profit after tax 1,400

———

350