Page 428 - Microsoft Word - 00 CIMA F1 Prelims STUDENT 2018.docx

P. 428

Chapter 20

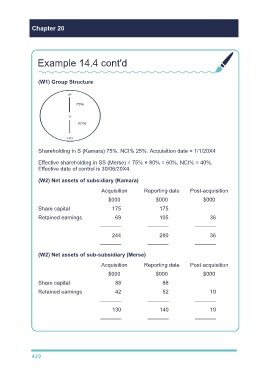

Example 14.4 cont'd

(W1) Group Structure

Shareholding in S (Kamara) 75%, NCI% 25%. Acquisition date = 1/1/20X4

Effective shareholding in SS (Merse) = 75% × 80% = 60%, NCI% = 40%.

Effective date of control is 30/06/20X4.

(W2) Net assets of subsidiary (Kamara)

Acquisition Reporting date Post-acquisition

$000 $000 $000

Share capital 175 175

Retained earnings 69 105 36

––––––– ––––––– –––––––

244 280 36

––––––– ––––––– –––––––

(W2) Net assets of sub-subsidiary (Merse)

Acquisition Reporting date Post-acquisition

$000 $000 $000

Share capital 88 88

Retained earnings 42 52 10

––––––– ––––––– –––––––

130 140 10

––––––– ––––––– –––––––

420