Page 440 - Microsoft Word - 00 CIMA F1 Prelims STUDENT 2018.docx

P. 440

Chapter 20

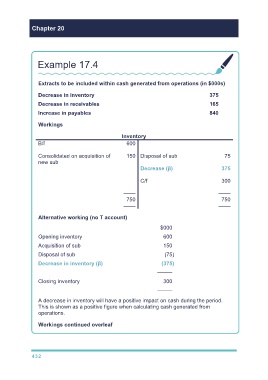

Example 17.4

Extracts to be included within cash generated from operations (in $000s)

Decrease in inventory 375

Decrease in receivables 165

Increase in payables 840

Workings

Inventory

B/f 600

Consolidated on acquisition of 150 Disposal of sub 75

new sub

Decrease (β) 375

C/f 300

–––– ––––

750 750

–––– ––––

Alternative working (no T account)

$000

Opening inventory 600

Acquisition of sub 150

Disposal of sub (75)

Decrease in inventory (β) (375)

–––––

Closing inventory 300

–––––

A decrease in inventory will have a positive impact on cash during the period.

This is shown as a positive figure when calculating cash generated from

operations.

Workings continued overleaf

432