Page 67 - Microsoft Word - 00 CIMA F1 Prelims STUDENT 2018.docx

P. 67

Financial instruments

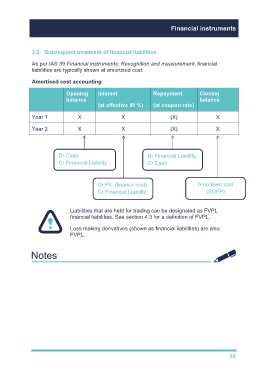

3.3 Subsequent treatment of financial liabilities

As per IAS 39 Financial instruments: Recognition and measurement, financial

liabilities are typically shown at amortised cost.

Amortised cost accounting

Opening Interest Repayment Closing

balance balance

(at effective IR %) (at coupon rate)

Year 1 X X (X) X

Year 2 X X (X) X

Dr Cash Dr Financial Liability

Cr Financial Liability Cr Cash

Dr P/L (finance cost) Amortised cost

Cr Financial Liability (SOFP)

Liabilities that are held for trading can be designated as FVPL

financial liabilities. See section 4.3 for a definition of FVPL.

Loss making derivatives (shown as financial liabilities) are also

FVPL.

59