Page 242 - BA2 Integrated Workbook STUDENT 2018

P. 242

Chapter 13

2.1 Breakeven point

An important concept for decision-makers is breakeven.

At a level of zero sales, the company’s total contribution will be zero therefore

they will make a total loss equal to the level of their fixed costs.

As sales revenues grow, the contribution will grow and will start to cover the fixed

costs. Eventually a point will be reached where neither profit nor loss is made, this is

the breakeven point. At this point the total contribution must exactly match the fixed

costs. Any additional contribution made above this level will constitute profit.

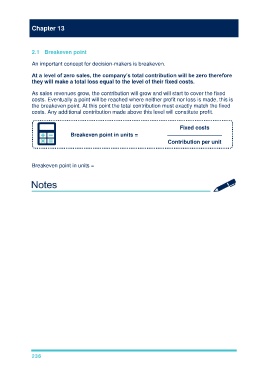

Fixed costs

Breakeven point in units = ————––—————

Contribution per unit

10,000

Breakeven point in units = ————— = 250 units

(120 – 80)

236