Page 19 - PowerPoint Presentation

P. 19

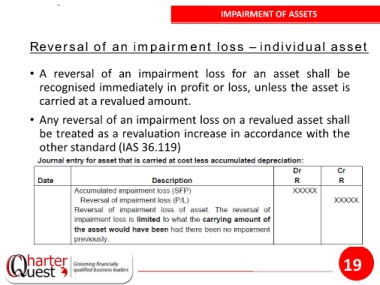

IMPAIRMENT OF ASSETS

Reversal of an impairment loss – individual asset

• A reversal of an impairment loss for an asset shall be

recognised immediately in profit or loss, unless the asset is

carried at a revalued amount.

• Any reversal of an impairment loss on a revalued asset shall

be treated as a revaluation increase in accordance with the

other standard (IAS 36.119)

19