Page 206 - F2 - MA Integrated Workbook STUDENT 2018-19

P. 206

Chapter 9

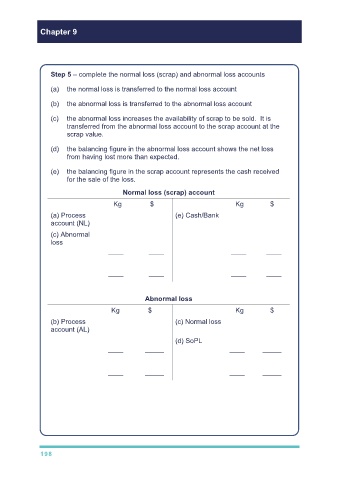

Step 5 – complete the normal loss (scrap) and abnormal loss accounts

(a) the normal loss is transferred to the normal loss account

(b) the abnormal loss is transferred to the abnormal loss account

(c) the abnormal loss increases the availability of scrap to be sold. It is

transferred from the abnormal loss account to the scrap account at the

scrap value.

(d) the balancing figure in the abnormal loss account shows the net loss

from having lost more than expected.

(e) the balancing figure in the scrap account represents the cash received

for the sale of the loss.

Normal loss (scrap) account

Kg $ Kg $

(a) Process 100 180 (e) Cash/Bank 200 360

account (NL)

(c) Abnormal 100 180

loss

–––– –––– –––– ––––

200 360 200 360

–––– –––– –––– ––––

Abnormal loss

Kg $ Kg $

(b) Process 100 2,280 (c) Normal loss 100 180

account (AL)

(d) SoPL 2,100

–––– ––––– –––– –––––

100 2,280 100 2,280

–––– ––––– –––– –––––

Note: the normal loss is sold for cash so the bank account is debited with the

normal loss proceeds of $180. The abnormal loss is also sold for scrap at

$1.80 per kg so a further 100 × $1.80 = $180 would be debited to the bank

account.

The net effect is that the abnormal loss is valued at $2,280 - $180 = $2,100

198