Page 324 - F2 - MA Integrated Workbook STUDENT 2018-19

P. 324

Chapter 13

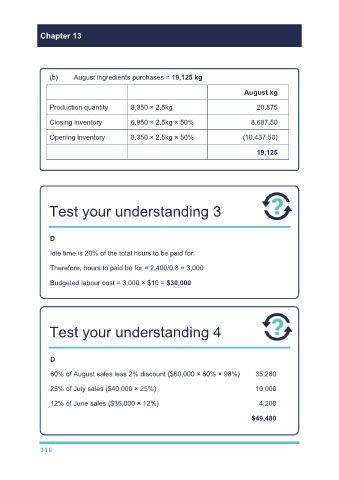

(b) August ingredients purchases = 19,125 kg

August kg

Production quantity 8,350 × 2.5kg 20,875

Closing inventory 6,950 × 2.5kg × 50% 8,687.50

Opening inventory 8,350 × 2.5kg × 50% (10,437.50)

19,125

Test your understanding 3

D

Idle time is 20% of the total hours to be paid for.

Therefore, hours to paid be for = 2,400/0.8 = 3,000

Budgeted labour cost = 3,000 × $10 = $30,000

Test your understanding 4

D

60% of August sales less 2% discount ($60,000 × 60% × 98%) 35,280

25% of July sales ($40,000 × 25%) 10,000

12% of June sales ($35,000 × 12%) 4,200

$49,480

316