Page 327 - F2 - MA Integrated Workbook STUDENT 2018-19

P. 327

Budgeting

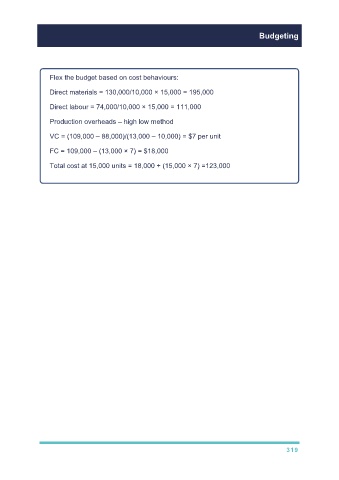

Flex the budget based on cost behaviours:

Direct materials = 130,000/10,000 × 15,000 = 195,000

Direct labour = 74,000/10,000 × 15,000 = 111,000

Production overheads – high low method

VC = (109,000 – 88,000)/(13,000 – 10,000) = $7 per unit

FC = 109,000 – (13,000 × 7) = $18,000

Total cost at 15,000 units = 18,000 + (15,000 × 7) =123,000

319