Page 481 - F2 - MA Integrated Workbook STUDENT 2018-19

P. 481

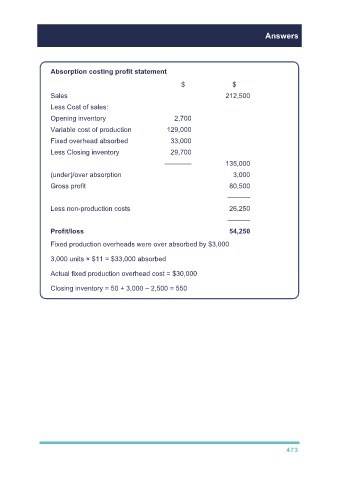

Answers

Absorption costing profit statement

$ $

Sales 212,500

Less Cost of sales:

Opening inventory 2,700

Variable cost of production 129,000

Fixed overhead absorbed 33,000

Less Closing inventory 29,700

––––––– 135,000

(under)/over absorption 3,000

Gross profit 80,500

––––––

Less non-production costs 26,250

––––––

Profit/loss 54,250

Fixed production overheads were over absorbed by $3,000

3,000 units × $11 = $33,000 absorbed

Actual fixed production overhead cost = $30,000

Closing inventory = 50 + 3,000 – 2,500 = 550

473