Page 132 - Microsoft Word - 00 ACCA F2 Prelims.docx

P. 132

Chapter 8

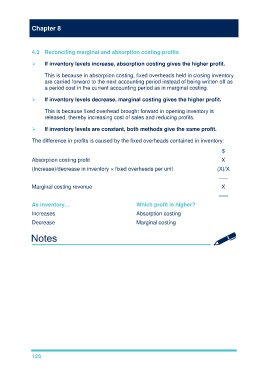

4.3 Reconciling marginal and absorption costing profits

If inventory levels increase, absorption costing gives the higher profit.

This is because in absorption costing, fixed overheads held in closing inventory

are carried forward to the next accounting period instead of being written off as

a period cost in the current accounting period as in marginal costing.

If inventory levels decrease, marginal costing gives the higher profit.

This is because fixed overhead brought forward in opening inventory is

released, thereby increasing cost of sales and reducing profits.

If inventory levels are constant, both methods give the same profit.

The difference in profits is caused by the fixed overheads contained in inventory:

$

Absorption costing profit X

(Increase)/decrease in inventory × fixed overheads per unit (X)/X

–––

Marginal costing revenue X

–––

As inventory... Which profit is higher?

Increases Absorption costing

Decrease Marginal costing

126