Page 14 - PowerPoint Presentation

P. 14

CONSOLIDATIONS AFTER THE DATE OF ACQUISITION

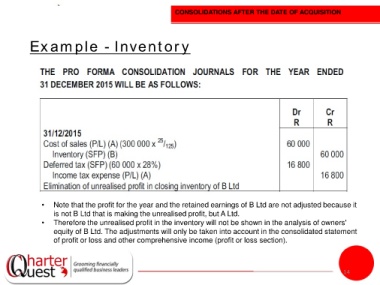

Example - Inventory

• Note that the profit for the year and the retained earnings of B Ltd are not adjusted because it

is not B Ltd that is making the unrealised profit, but A Ltd.

• Therefore the unrealised profit in the inventory will not be shown in the analysis of owners'

equity of B Ltd. The adjustments will only be taken into account in the consolidated statement

of profit or loss and other comprehensive income (profit or loss section).

14