Page 17 - FINAL CFA SLIDES DECEMBER 2018 DAY 12

P. 17

Session Unit 12:

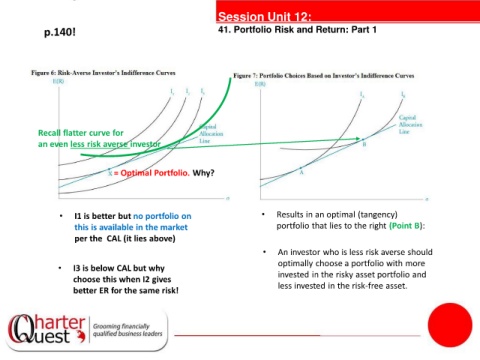

p.140! 41. Portfolio Risk and Return: Part 1

Recall flatter curve for

an even less risk averse investor

tanties

= Optimal Portfolio. Why?

• I1 is better but no portfolio on • Results in an optimal (tangency)

this is available in the market portfolio that lies to the right (Point B):

per the CAL (it lies above)

• An investor who is less risk averse should

• I3 is below CAL but why optimally choose a portfolio with more

choose this when I2 gives invested in the risky asset portfolio and

less invested in the risk-free asset.

better ER for the same risk!