Page 23 - FINAL CFA SLIDES DECEMBER 2018 DAY 3

P. 23

Session Unit 2:

8. Statistical Concepts and Market Returns

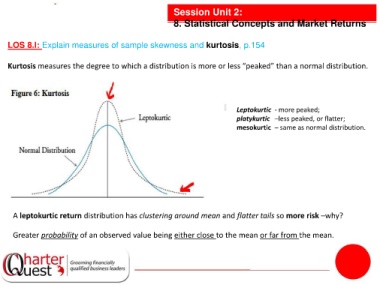

LOS 8.l: Explain measures of sample skewness and kurtosis, p.154

Kurtosis measures the degree to which a distribution is more or less “peaked” than a normal distribution.

Leptokurtic - more peaked;

platykurtic –less peaked, or flatter;

mesokurtic – same as normal distribution.

A leptokurtic return distribution has clustering around mean and flatter tails so more risk –why?

Greater probability of an observed value being either close to the mean or far from the mean.