Page 17 - F6 - Capital Gains Tax - Assets & Disposals

P. 17

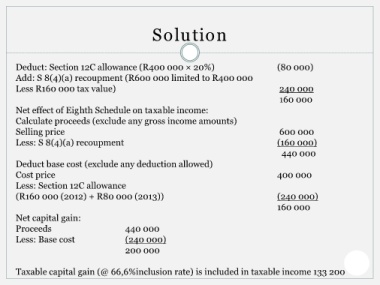

Solution

Deduct: Section 12C allowance (R400 000 × 20%) (80 000)

Add: S 8(4)(a) recoupment (R600 000 limited to R400 000

Less R160 000 tax value) 240 000

160 000

Net effect of Eighth Schedule on taxable income:

Calculate proceeds (exclude any gross income amounts)

Selling price 600 000

Less: S 8(4)(a) recoupment (160 000)

440 000

Deduct base cost (exclude any deduction allowed)

Cost price 400 000

Less: Section 12C allowance

(R160 000 (2012) + R80 000 (2013)) (240 000)

160 000

Net capital gain:

Proceeds 440 000

Less: Base cost (240 000)

200 000

Taxable capital gain (@ 66,6%inclusion rate) is included in taxable income 133 200