Page 40 - Test 1 Slides - 4. Gross Income

P. 40

GROSS INCOME

Example – application of physical

presence test

Solution:

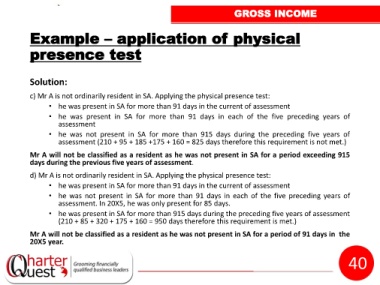

c) Mr A is not ordinarily resident in SA. Applying the physical presence test:

• he was present in SA for more than 91 days in the current of assessment

• he was present in SA for more than 91 days in each of the five preceding years of

assessment

• he was not present in SA for more than 915 days during the preceding five years of

assessment (210 + 95 + 185 +175 + 160 = 825 days therefore this requirement is not met.)

Mr A will not be classified as a resident as he was not present in SA for a period exceeding 915

days during the previous five years of assessment.

d) Mr A is not ordinarily resident in SA. Applying the physical presence test:

• he was present in SA for more than 91 days in the current of assessment

• he was not present in SA for more than 91 days in each of the five preceding years of

assessment. In 20X5, he was only present for 85 days.

• he was present in SA for more than 915 days during the preceding five years of assessment

(210 + 85 + 320 + 175 + 160 = 950 days therefore this requirement is met.)

Mr A will not be classified as a resident as he was not present in SA for a period of 91 days in the

20X5 year.

40