Page 195 - F2 Integrated Workbook STUDENT 2019

P. 195

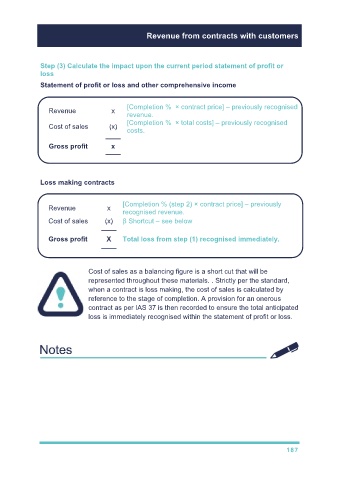

Revenue from contracts with customers

Step (3) Calculate the impact upon the current period statement of profit or

loss

Statement of profit or loss and other comprehensive income

[Completion % × contract price] – previously recognised

Revenue x

revenue.

[Completion % × total costs] – previously recognised

Cost of sales (x)

costs.

––––

Gross profit x

––––

Loss making contracts

[Completion % (step 2) × contract price] – previously

Revenue x

recognised revenue.

Cost of sales (x) β Shortcut – see below

––––

Gross profit X Total loss from step (1) recognised immediately.

––––

Cost of sales as a balancing figure is a short cut that will be

represented throughout these materials. . Strictly per the standard,

when a contract is loss making, the cost of sales is calculated by

reference to the stage of completion. A provision for an onerous

contract as per IAS 37 is then recorded to ensure the total anticipated

loss is immediately recognised within the statement of profit or loss.

187