Page 418 - F2 Integrated Workbook STUDENT 2019

P. 418

Chapter 19

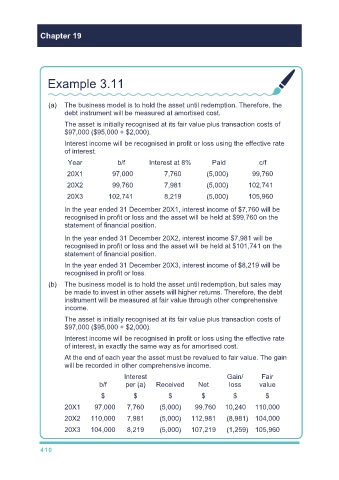

Example 3.11

(a) The business model is to hold the asset until redemption. Therefore, the

debt instrument will be measured at amortised cost.

The asset is initially recognised at its fair value plus transaction costs of

$97,000 ($95,000 + $2,000).

Interest income will be recognised in profit or loss using the effective rate

of interest.

Year b/f Interest at 8% Paid c/f

20X1 97,000 7,760 (5,000) 99,760

20X2 99,760 7,981 (5,000) 102,741

20X3 102,741 8,219 (5,000) 105,960

In the year ended 31 December 20X1, interest income of $7,760 will be

recognised in profit or loss and the asset will be held at $99,760 on the

statement of financial position.

In the year ended 31 December 20X2, interest income $7,981 will be

recognised in profit or loss and the asset will be held at $101,741 on the

statement of financial position.

In the year ended 31 December 20X3, interest income of $8,219 will be

recognised in profit or loss.

(b) The business model is to hold the asset until redemption, but sales may

be made to invest in other assets will higher returns. Therefore, the debt

instrument will be measured at fair value through other comprehensive

income.

The asset is initially recognised at its fair value plus transaction costs of

$97,000 ($95,000 + $2,000).

Interest income will be recognised in profit or loss using the effective rate

of interest, in exactly the same way as for amortised cost.

At the end of each year the asset must be revalued to fair value. The gain

will be recorded in other comprehensive income.

Interest Gain/ Fair

b/f per (a) Received Net loss value

$ $ $ $ $ $

20X1 97,000 7,760 (5,000) 99,760 10,240 110,000

20X2 110,000 7,981 (5,000) 112,981 (8,981) 104,000

20X3 104,000 8,219 (5,000) 107,219 (1,259) 105,960

410