Page 378 - F3 -FA Integrated Workbook STUDENT 2018-19

P. 378

Chapter 24

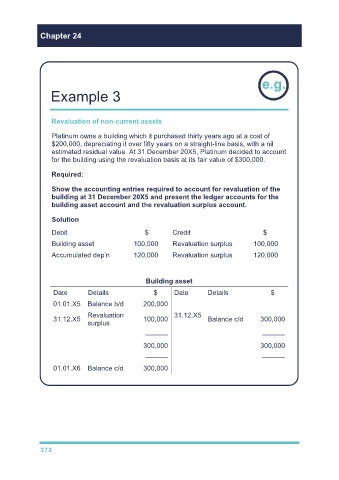

Example 3

Revaluation of non-current assets

Platinum owns a building which it purchased thirty years ago at a cost of

$200,000, depreciating it over fifty years on a straight-line basis, with a nil

estimated residual value. At 31 December 20X5, Platinum decided to account

for the building using the revaluation basis at its fair value of $300,000.

Required:

Show the accounting entries required to account for revaluation of the

building at 31 December 20X5 and present the ledger accounts for the

building asset account and the revaluation surplus account.

Solution

Debit $ Credit $

Building asset 100,000 Revaluation surplus 100,000

Accumulated dep’n 120,000 Revaluation surplus 120,000

Building asset

Date Details $ Date Details $

01.01.X5 Balance b/d 200,000

Revaluation 31.12.X5

31.12.X5 100,000 Balance c/d 300,000

surplus

–––––– ––––––

300,000 300,000

–––––– ––––––

01.01.X6 Balance c/d 300,000

372