Page 376 - F3 -FA Integrated Workbook STUDENT 2018-19

P. 376

Chapter 24

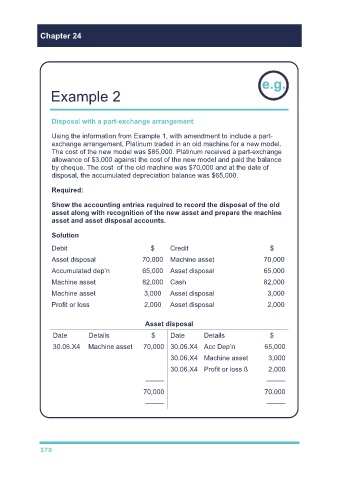

Example 2

Disposal with a part-exchange arrangement

Using the information from Example 1, with amendment to include a part-

exchange arrangement, Platinum traded in an old machine for a new model.

The cost of the new model was $85,000. Platinum received a part-exchange

allowance of $3,000 against the cost of the new model and paid the balance

by cheque. The cost of the old machine was $70,000 and at the date of

disposal, the accumulated depreciation balance was $65,000.

Required:

Show the accounting entries required to record the disposal of the old

asset along with recognition of the new asset and prepare the machine

asset and asset disposal accounts.

Solution

Debit $ Credit $

Asset disposal 70,000 Machine asset 70,000

Accumulated dep’n 65,000 Asset disposal 65,000

Machine asset 82,000 Cash 82,000

Machine asset 3,000 Asset disposal 3,000

Profit or loss 2,000 Asset disposal 2,000

Asset disposal

Date Details $ Date Details $

30.06.X4 Machine asset 70,000 30.06.X4 Acc Dep’n 65,000

30.06.X4 Machine asset 3,000

30.06.X4 Profit or loss ß 2,000

––––– –––––

70,000 70,000

––––– –––––

370