Page 371 - F3 -FA Integrated Workbook STUDENT 2018-19

P. 371

Answers

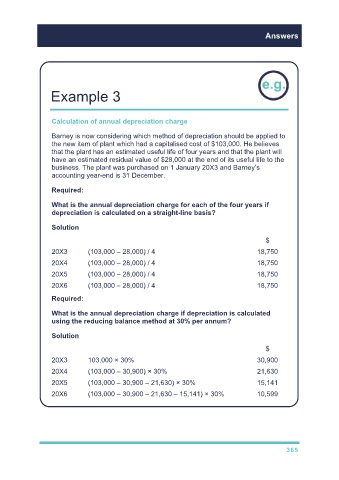

Example 3

Calculation of annual depreciation charge

Barney is now considering which method of depreciation should be applied to

the new item of plant which had a capitalised cost of $103,000. He believes

that the plant has an estimated useful life of four years and that the plant will

have an estimated residual value of $28,000 at the end of its useful life to the

business. The plant was purchased on 1 January 20X3 and Barney’s

accounting year-end is 31 December.

Required:

What is the annual depreciation charge for each of the four years if

depreciation is calculated on a straight-line basis?

Solution

$

20X3 (103,000 – 28,000) / 4 18,750

20X4 (103,000 – 28,000) / 4 18,750

20X5 (103,000 – 28,000) / 4 18,750

20X6 (103,000 – 28,000) / 4 18,750

Required:

What is the annual depreciation charge if depreciation is calculated

using the reducing balance method at 30% per annum?

Solution

$

20X3 103,000 × 30% 30,900

20X4 (103,000 – 30,900) × 30% 21,630

20X5 (103,000 – 30,900 – 21,630) × 30% 15,141

20X6 (103,000 – 30,900 – 21,630 – 15,141) × 30% 10,599

365