Page 368 - F3 -FA Integrated Workbook STUDENT 2018-19

P. 368

Chapter 24

Chapter 6

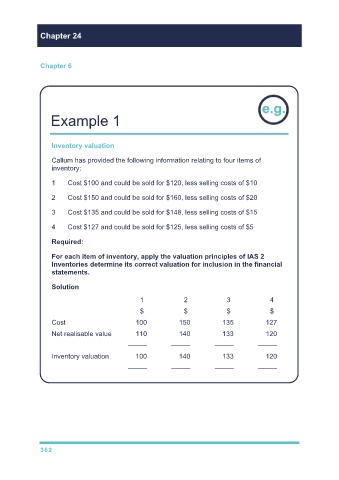

Example 1

Inventory valuation

Callum has provided the following information relating to four items of

inventory:

1 Cost $100 and could be sold for $120, less selling costs of $10

2 Cost $150 and could be sold for $160, less selling costs of $20

3 Cost $135 and could be sold for $148, less selling costs of $15

4 Cost $127 and could be sold for $125, less selling costs of $5

Required:

For each item of inventory, apply the valuation principles of IAS 2

Inventories determine its correct valuation for inclusion in the financial

statements.

Solution

1 2 3 4

$ $ $ $

Cost 100 150 135 127

Net realisable value 110 140 133 120

––––– ––––– ––––– –––––

Inventory valuation 100 140 133 120

––––– ––––– ––––– –––––

362