Page 280 - P1 Integrated Workbook STUDENT 2018

P. 280

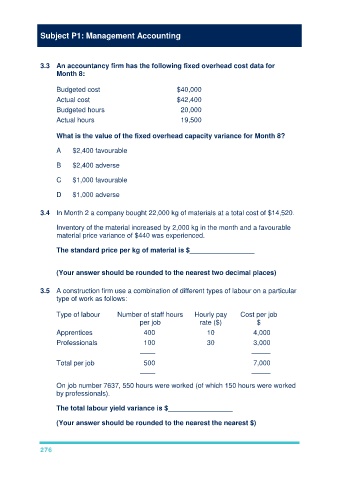

Subject P1: Management Accounting

3.3 An accountancy firm has the following fixed overhead cost data for

Month 8:

Budgeted cost $40,000

Actual cost $42,400

Budgeted hours 20,000

Actual hours 19,500

What is the value of the fixed overhead capacity variance for Month 8?

A $2,400 favourable

B $2,400 adverse

C $1,000 favourable

D $1,000 adverse

3.4 In Month 2 a company bought 22,000 kg of materials at a total cost of $14,520.

Inventory of the material increased by 2,000 kg in the month and a favourable

material price variance of $440 was experienced.

The standard price per kg of material is $_________________

(Your answer should be rounded to the nearest two decimal places)

3.5 A construction firm use a combination of different types of labour on a particular

type of work as follows:

Type of labour Number of staff hours Hourly pay Cost per job

per job rate ($) $

Apprentices 400 10 4,000

Professionals 100 30 3,000

–––– –––––

Total per job 500 7,000

–––– –––––

On job number 7637, 550 hours were worked (of which 150 hours were worked

by professionals).

The total labour yield variance is $_________________

(Your answer should be rounded to the nearest the nearest $)

276