Page 19 - Microsoft Word - 00 Prelims.docx

P. 19

A revision of F2 topics

Traditional costing methods

2.1 Absorption costing

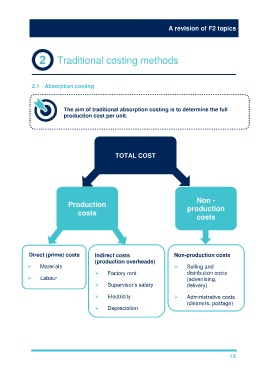

The aim of traditional absorption costing is to determine the full

production cost per unit.

TOTAL COST

Non -

Production

production

costs

costs

Direct (prime) costs Indirect costs Non-production costs

(production overheads)

Materials Selling and

Factory rent distribution costs

Labour (advertising,

Supervisor’s salary delivery)

Electricity Administrative costs

(cleaners, postage)

Depreciation

13