Page 253 - Microsoft Word - 00 BA3 IW Prelims STUDENT.docx

P. 253

Accounting for inventory

Valuation of inventory

3.1 IAS 2 Inventories

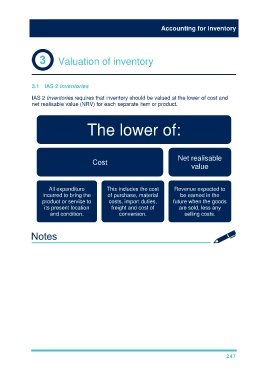

IAS 2 Inventories requires that inventory should be valued at the lower of cost and

net realisable value (NRV) for each separate item or product.

The lower of:

Net realisable

Cost

value

All expenditure This includes the cost Revenue expected to

incurred to bring the of purchase, material be earned in the

product or service to costs, import duties, future when the goods

its present location freight and cost of are sold, less any

and condition. conversion. selling costs.

247