Page 376 - Microsoft Word - 00 BA3 IW Prelims STUDENT.docx

P. 376

Chapter 20

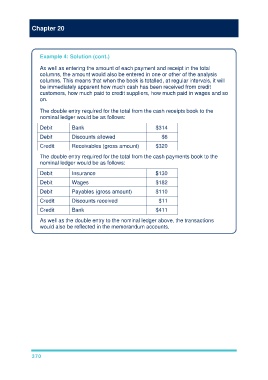

Example 4: Solution (cont.)

As well as entering the amount of each payment and receipt in the total

columns, the amount would also be entered in one or other of the analysis

columns. This means that when the book is totalled, at regular intervals, it will

be immediately apparent how much cash has been received from credit

customers, how much paid to credit suppliers, how much paid in wages and so

on.

The double entry required for the total from the cash receipts book to the

nominal ledger would be as follows:

Debit Bank $314

Debit Discounts allowed $6

Credit Receivables (gross amount) $320

The double entry required for the total from the cash payments book to the

nominal ledger would be as follows:

Debit Insurance $130

Debit Wages $182

Debit Payables (gross amount) $110

Credit Discounts received $11

Credit Bank $411

As well as the double entry to the nominal ledger above, the transactions

would also be reflected in the memorandum accounts.

370