Page 4 - FINAL CFA II SLIDES JUNE 2019 DAY 8

P. 4

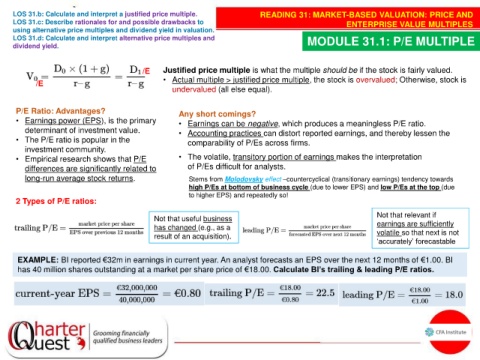

LOS 31.b: Calculate and interpret a justified price multiple. READING 31: MARKET-BASED VALUATION: PRICE AND

LOS 31.c: Describe rationales for and possible drawbacks to ENTERPRISE VALUE MULTIPLES

using alternative price multiples and dividend yield in valuation.

LOS 31.d: Calculate and interpret alternative price multiples and MODULE 31.1: P/E MULTIPLE

dividend yield.

/E Justified price multiple is what the multiple should be if the stock is fairly valued.

/E • Actual multiple > justified price multiple, the stock is overvalued; Otherwise, stock is

undervalued (all else equal).

P/E Ratio: Advantages? Any short comings?

• Earnings power (EPS), is the primary • Earnings can be negative, which produces a meaningless P/E ratio.

determinant of investment value. • Accounting practices can distort reported earnings, and thereby lessen the

• The P/E ratio is popular in the comparability of P/Es across firms.

investment community.

• Empirical research shows that P/E • The volatile, transitory portion of earnings makes the interpretation

differences are significantly related to of P/Es difficult for analysts.

long-run average stock returns. Stems from Molodovsky effect –countercyclical (transitionary earnings) tendency towards

high P/Es at bottom of business cycle (due to lower EPS) and low P/Es at the top (due

to higher EPS) and repeatedly so!

2 Types of P/E ratios:

Not that relevant if

Not that useful business

has changed (e.g., as a earnings are sufficiently

result of an acquisition). volatile so that next is not

‘accurately’ forecastable

EXAMPLE: BI reported €32m in earnings in current year. An analyst forecasts an EPS over the next 12 months of €1.00. BI

has 40 million shares outstanding at a market per share price of €18.00. Calculate BI’s trailing & leading P/E ratios.