Page 126 - Microsoft Word - 00 P1 IW Prelims.docx

P. 126

Chapter 9

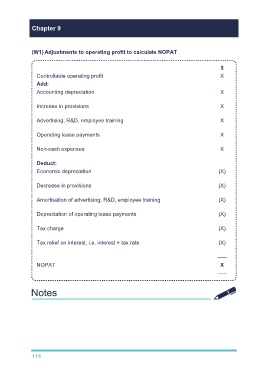

(W1) Adjustments to operating profit to calculate NOPAT

$

Controllable operating profit X

Add:

Accounting depreciation X

(does not represent true fall in value of assets in the period)

Increase in provisions X

(over prudence and not a cash figure)

Advertising, R&D, employee training X

(can capitalise since add value)

Operating lease payments X

(can capitalise since add value)

Non-cash expenses X

(not actual cash paid)

Deduct:

Economic depreciation (X)

(reflects true fall in value of assets in the period)

Decrease in provisions (X)

(over prudence and not a cash figure)

Amortisation of advertising, R&D, employee training (X)

(amortisation for the period)

Depreciation of operating lease payments (X)

(depreciation for the period)

Tax charge (X)

(want after tax profit)

Tax relief on interest, i.e. interest × tax rate (X)

(interest payments taken into account in WACC)

–––

NOPAT X

–––

116