Page 212 - Microsoft Word - 00 CIMA F1 Prelims STUDENT 2018.docx

P. 212

Subject P2: Advanced Management Accounting

CHAPTER 3 – COSTING TECHNIQUES

3.1 B

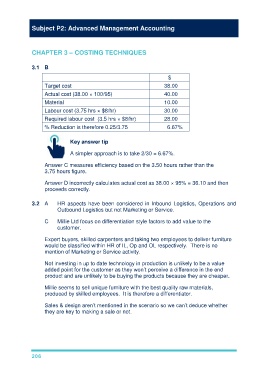

$

Target cost 38.00

Actual cost (38.00 × 100/95) 40.00

Material 10.00

Labour cost (3.75 hrs × $8/hr) 30.00

Required labour cost (3.5 hrs × $8/hr) 28.00

% Reduction is therefore 0.25/3.75 6.67%

Key answer tip

A simpler approach is to take 2/30 = 6.67%.

Answer C measures efficiency based on the 3.50 hours rather than the

3.75 hours figure.

Answer D incorrectly calculates actual cost as 38.00 × 95% = 36.10 and then

proceeds correctly.

3.2 A HR aspects have been considered in Inbound Logistics, Operations and

Outbound Logistics but not Marketing or Service.

C Millie Ltd focus on differentiation style factors to add value to the

customer.

Expert buyers, skilled carpenters and taking two employees to deliver furniture

would be classified within HR of IL, Op and OL respectively. There is no

mention of Marketing or Service activity.

Not investing in up to date technology in production is unlikely to be a value

added point for the customer as they won’t perceive a difference in the end

product and are unlikely to be buying the products because they are cheaper.

Millie seems to sell unique furniture with the best quality raw materials,

produced by skilled employees. It is therefore a differentiator.

Sales & design aren’t mentioned in the scenario so we can’t deduce whether

they are key to making a sale or not.

206