Page 88 - Microsoft Word - 00 CIMA F1 Prelims STUDENT 2018.docx

P. 88

Chapter 8

The tabular approach

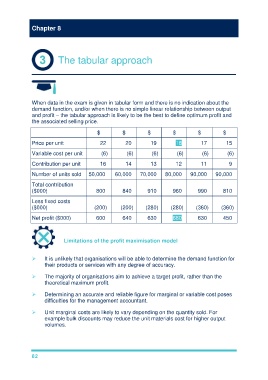

When data in the exam is given in tabular form and there is no indication about the

demand function, and/or when there is no simple linear relationship between output

and profit – the tabular approach is likely to be the best to define optimum profit and

the associated selling price.

$ $ $ $ $ $

Price per unit 22 20 19 18 17 15

Variable cost per unit (6) (6) (6) (6) (6) (6)

Contribution per unit 16 14 13 12 11 9

Number of units sold 50,000 60,000 70,000 80,000 90,000 90,000

Total contribution

($000) 800 840 910 960 990 810

Less fixed costs

($000) (200) (200) (280) (280) (360) (360)

Net profit ($000) 600 640 630 680 630 450

Limitations of the profit maximisation model

It is unlikely that organisations will be able to determine the demand function for

their products or services with any degree of accuracy.

The majority of organisations aim to achieve a target profit, rather than the

theoretical maximum profit.

Determining an accurate and reliable figure for marginal or variable cost poses

difficulties for the management accountant.

Unit marginal costs are likely to vary depending on the quantity sold. For

example bulk discounts may reduce the unit materials cost for higher output

volumes.

82