Page 234 - pwc-lease-accounting-guide_Neat

P. 234

Sale and leaseback transactions

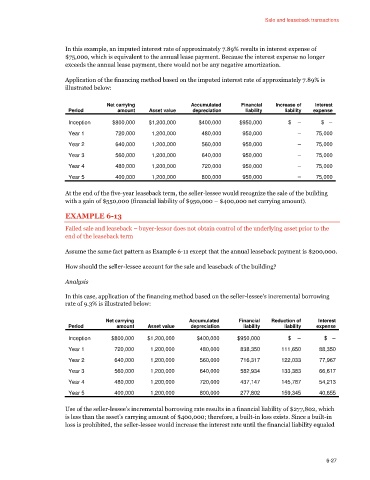

In this example, an imputed interest rate of approximately 7.89% results in interest expense of

$75,000, which is equivalent to the annual lease payment. Because the interest expense no longer

exceeds the annual lease payment, there would not be any negative amortization.

Application of the financing method based on the imputed interest rate of approximately 7.89% is

illustrated below:

Net carrying Accumulated Financial Increase of Interest

Period amount Asset value depreciation liability liability expense

Inception $800,000 $1,200,000 $400,000 $950,000 $ – $ –

Year 1 720,000 1,200,000 480,000 950,000 – 75,000

Year 2 640,000 1,200,000 560,000 950,000 – 75,000

Year 3 560,000 1,200,000 640,000 950,000 – 75,000

Year 4 480,000 1,200,000 720,000 950,000 – 75,000

Year 5 400,000 1,200,000 800,000 950,000 – 75,000

At the end of the five-year leaseback term, the seller-lessee would recognize the sale of the building

with a gain of $550,000 (financial liability of $950,000 – $400,000 net carrying amount).

EXAMPLE 6-13

Failed sale and leaseback – buyer-lessor does not obtain control of the underlying asset prior to the

end of the leaseback term

Assume the same fact pattern as Example 6-11 except that the annual leaseback payment is $200,000.

How should the seller-lessee account for the sale and leaseback of the building?

Analysis

In this case, application of the financing method based on the seller-lessee’s incremental borrowing

rate of 9.3% is illustrated below:

Net carrying Accumulated Financial Reduction of Interest

Period amount Asset value depreciation liability liability expense

Inception $800,000 $1,200,000 $400,000 $950,000 $ – $ –

Year 1 720,000 1,200,000 480,000 838,350 111,650 88,350

Year 2 640,000 1,200,000 560,000 716,317 122,033 77,967

Year 3 560,000 1,200,000 640,000 582,934 133,383 66,617

Year 4 480,000 1,200,000 720,000 437,147 145,787 54,213

Year 5 400,000 1,200,000 800,000 277,802 159,345 40,655

Use of the seller-lessee’s incremental borrowing rate results in a financial liability of $277,802, which

is less than the asset’s carrying amount of $400,000; therefore, a built-in loss exists. Since a built-in

loss is prohibited, the seller-lessee would increase the interest rate until the financial liability equaled

6-27