Page 141 - RB GRENADA ANNUAL REPORT 2025_ONLINE

P. 141

• 141

Notes to the Financial Statements

For the year ended September 30, 2025. Expressed in Thousands of Eastern Caribbean dollars ($’000), except where otherwise stated.

20 Capital management

For the purpose of the Bank’s capital management, capital includes issued share capital and other equity reserves. The Bank’s

policy is to diversify its sources of capital, to allocate capital within the Bank efficiently and to maintain a prudent relationship

between capital resources and the risk of its underlying business. Equity increased by $ 7.70 million to $260.19 million during

the year under review. This was mainly as a result of profit after tax of $15.42 million for fiscal 2025, a reduction of $0.43 million

in defined benefit reserve and dividend paid of $7.36 million.

Capital adequacy is monitored by the Bank, employing techniques based on the guidelines developed by the Basel Committee

on Banking Regulations and Supervisory Practice (the Basel Committee), as implemented by the Eastern Caribbean Central

Bank for supervisory purposes. The Basel risk-based capital guidelines require a minimum ratio of core capital (Tier 1) to risk-

weighted assets of 4 percent, with a minimum total qualifying capital (Tier 2) ratio of 8 percent. Core capital (Tier 1) comprises

mainly shareholders’ equity.

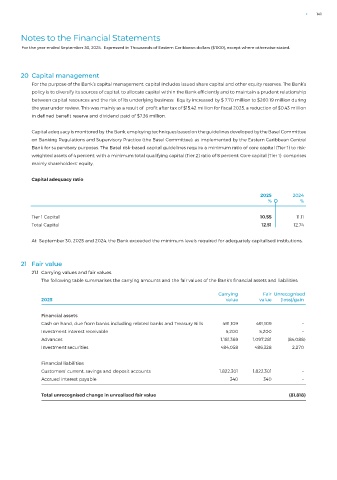

Capital adequacy ratio

2025 2024

% %

Tier 1 Capital 10.55 11.11

Total Capital 12.51 12.74

At September 30, 2025 and 2024, the Bank exceeded the minimum levels required for adequately capitalised institutions.

21 Fair value

21.1 Carrying values and fair values

The following table summarises the carrying amounts and the fair values of the Bank’s financial assets and liabilities:

Carrying Fair Unrecognised

2025 value value (loss)/gain

Financial assets

Cash on hand, due from banks including related banks and Treasury Bills 491,109 491,109 –

Investment interest receivable 5,200 5,200 –

Advances 1,181,369 1,097,281 (84,088)

Investment securities 484,058 486,328 2,270

Financial liabilities

Customers’ current, savings and deposit accounts 1,822,301 1,822,301 –

Accrued interest payable 340 340 –

Total unrecognised change in unrealised fair value (81,818)