Page 15 - iA Excellence -Field Underwriting Guide - Updated on July 2019

P. 15

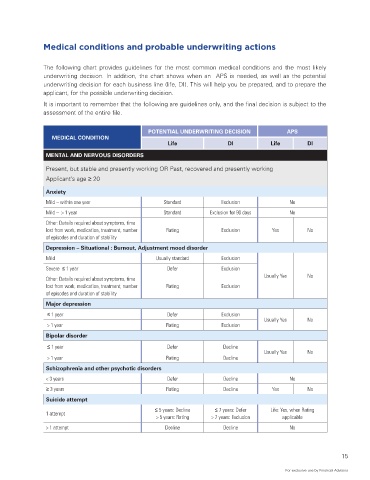

Medical conditions and probable underwriting actions

The following chart provides guidelines for the most common medical conditions and the most likely

underwriting decision. In addition, the chart shows when an APS is needed, as well as the potential

underwriting decision for each business line (life, DI). This will help you be prepared, and to prepare the

applicant, for the possible underwriting decision.

It is important to remember that the following are guidelines only, and the final decision is subject to the

assessment of the entire file.

POTENTIAL UNDERWRITING DECISION APS

MEDICAL CONDITION

Life DI Life DI

MENTAL AND NERVOUS DISORDERS

Present, but stable and presently working OR Past, recovered and presently working

Applicant’s age ≥ 20

Anxiety

Mild – within one year Standard Exclusion No

Mild – > 1 year Standard Exclusion for 90 days No

Other: Details required about symptoms, time

lost from work, medication, treatment, number Rating Exclusion Yes No

of episodes and duration of stability

Depression – Situational : Burnout, Adjustment mood disorder

Mild Usually standard Exclusion

Severe ≤ 1 year Defer Exclusion

Usually Yes No

Other: Details required about symptoms, time

lost from work, medication, treatment, number Rating Exclusion

of episodes and duration of stability

Major depression

≤ 1 year Defer Exclusion

Usually Yes No

> 1 year Rating Exclusion

Bipolar disorder

≤ 1 year Defer Decline

Usually Yes No

> 1 year Rating Decline

Schizophrenia and other psychotic disorders

< 3 years Defer Decline No

≥ 3 years Rating Decline Yes No

Suicide attempt

≤ 5 years: Decline ≤ 7 years: Defer Life: Yes, when Rating

1 attempt

> 5 years: Rating > 7 years: Exclusion applicable

> 1 attempt Decline Decline No

15

For exclusive use by Financial Advisors