Page 50 - ASBIRES-2017_Preceedings

P. 50

AN IDENTIFICATION OF KEY PERFORMANCE INDICATORS FOR MEASURING ORGANIZATIONAL

PERFORMANCE IN TEAM LEADER BASED ORGANIZATION CULTURAL CONTEXT: A CASE STUDY

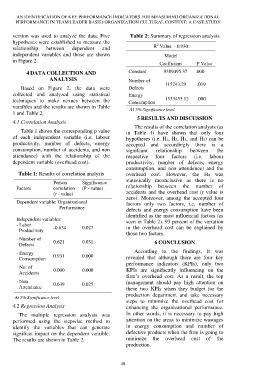

version was used to analyze the data. Five Table 2: Summary of regression analysis

hypotheses were established to measure the 2

relationship between dependent and R Value - 0.930

independent variables and those are shown Model

in Figure 2.

Coefficient P Value

4 DATA COLLECTION AND Constant 9389495.37 .000

ANALYSIS Number of

Based on Figure 2, the data were Defects 115243.29 .019

collected and analyzed using statistical Energy

techniques to make nexues between the Consumption 1533455.12 .000

varaibles and the results are shown in Table At 5% Significance level

1 and Table 2.

5 RESULTS AND DISCUSSION

4.1 Correlation Analysis

The results of the correlation analysis (as

Table 1 shows the corresponding p value in Table 1) have shown that only four

of each independent variable (i.e. labour hypotheses (i.e. H1, H2, H3, and H5) can be

productivity, number of defects, energy accepted and accordingly there is a

consumption, number of accidents, and non signifcant relationship between the

attendance) with the relationship of the respective four factors (i.e. labour

dependent variable (overhead cost). productivity, number of defects, energy

consumption, and non attendence) and the

Table 1: Results of correlation analysis overhead cost. However, the H4 was

statistically inconclusive as there is no

Person Significance

Factors correlation (P - value) relationship between the number of

(r - value) accidents and the overhead cost (r value is

zero). Moreover, among the accepted four

Dependent variable: Organizational factors only two factors, i.e. number of

Performance defects and energy consumption have been

identified as the most influencial factors (as

Independent variables: seen in Table 2). 93 percent of the variation

- Labor

Productivity -0.634 0.027 in the overhead cost can be explained by

those two factors.

- Number of 0.621 0.031

Defects 6 CONCLUSION

- Energy 0.931 0.000 According to the findings, it was

Consumption revealed that although there are four key

performance indicators (KPIs), only two

- No: of

Accidents 0.000 0.000 KPIs are signifacntly influencing on the

firm’s overhead cost. As a result, the top

- Non management should pay high attention on

Attendance 0.639 0.025 these two KPIs when they budget for the

production department and take necessary

At 5% Significance level

steps to minimize the overhead cost for

4.2 Regression Analysis enhancing the organizational performance.

The multiple regression analysis was In other words, it is necessary to pay high

performed using the stepwise method to attention on the areas to minimize wastages

identify the variables that can generate in energy consumption and number of

significat impact on the dependent varaible. defective products when the firm is going to

The results are shown in Table 2. minimize the overhead cost of the

production.

40