Page 14 - cfi-Accounting-eBook

P. 14

The Corporate Finance Institute Accounting

For asset accounts, which include cash, accounts receivable, inventory,

PP&E, and others, the left side of the T-Account (debit side) is always

an increase to the account. The right side (credit side) is conversely, a

decrease to the asset account. For liabilities and equity accounts, the

debit and credit sides of the T-Account are the same, however, the debit

side signifies a decrease to the account and the credit side signifies an

increase to the account.

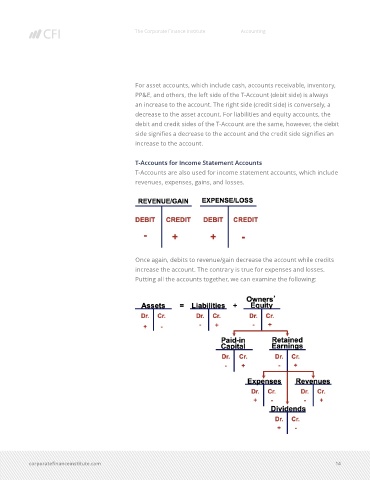

T-Accounts for Income Statement Accounts

T-Accounts are also used for income statement accounts, which include

revenues, expenses, gains, and losses.

Once again, debits to revenue/gain decrease the account while credits

increase the account. The contrary is true for expenses and losses.

Putting all the accounts together, we can examine the following:

corporatefinanceinstitute.com 14