Page 161 - คู่มือการเขียนวิจัยและการอ้างอิง

P. 161

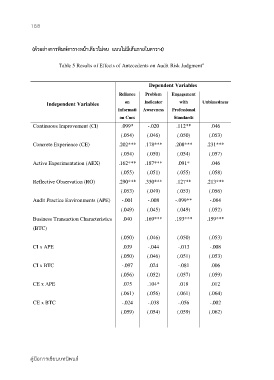

158

(ตัวอยางการพิมพตารางหนาเดียวไมจบ แบบไมมีเสนภายในตาราง)

Table 5 Results of Effects of Antecedents on Audit Risk Judgment a

Dependent Variables

Reliance Problem Engagement

Independent Variables on Indicator with Unbiasedness

Informati Awareness Professional

on Cues Standards

Continuous Improvement (CI) .099* -.020 .112** .046

(.054) (.046) (.050) (.053)

Concrete Experience (CE) .202*** .178*** .208*** .231***

(.054) (.050) (.054) (.057)

Active Experimentation (AEX) .162*** .187*** .091* .046

(.055) (.051) (.055) (.058)

Reflective Observation (RO) .290*** .330*** .127** .213***

(.053) (.049) (.053) (.056)

Audit Practice Environments (APE) -.001 -.008 -.099** -.084

(.049) (.045) (.049) (.052)

Business Transaction Characteristics .040 .169*** .193*** .159***

(BTC)

(.050) (.046) (.050) (.053)

CI x APE .039 -.044 -.013 -.008

(.050) (.046) (.051) (.053)

CI x BTC -.097 .024 -.081 .006

(.056) (.052) (.057) (.059)

CE x APE .075 .104* .018 .012

(.061) (.056) (.061) (.064)

CE x BTC -.024 -.038 -.056 -.002

(.059) (.054) (.059) (.062)

คูมือการเขียนบทนิพนธ