Page 256 - JoFA_2022

P. 256

TAX

Scenario 3: A day trader, who qualifies as a trader in discuss both how the client can qualify as a trader

securities, has net realized short-term gains from sales in securities and the differences between the tax

of securities during 2021 of $10,000, has $10,000 of treatment of trading activities with and without a

trading expenses, and holds securities at the close of the Sec. 475(f) election. The election is a two-edged

year on which a net gain of $20,000 would be realized sword, and depending on the client’s circum-

if they were sold for FMV. The trader also receives stances during a year, may increase or decrease his

$95,000 of ordinary income from other sources and or her tax liability. Moreover, the election must be

takes the standard deduction. Notice that by making the made in the year prior to being effective and once

Sec. 475(f) mark-to-market election, both the realized made can only be revoked with the IRS’s consent.

and unrealized gain become part of ordinary income. Therefore, to determine if making a Sec. 475(f)

election will be beneficial, the client must realisti-

ADVISING DAY TRADER CLIENTS cally consider what his or her tax circumstances

When advising a client who day-trades or anticipates are likely to be in both the year the election

doing so in the future, a practitioner should be sure to becomes effective and future years. ■

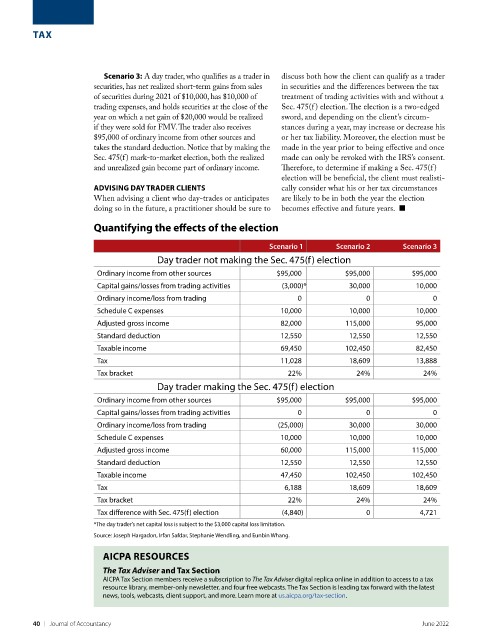

Quantifying the effects of the election

Scenario 1 Scenario 2 Scenario 3

Day trader not making the Sec. 475(f) election

Ordinary income from other sources $95,000 $95,000 $95,000

Capital gains/losses from trading activities (3,000)* 30,000 10,000

Ordinary income/loss from trading 0 0 0

Schedule C expenses 10,000 10,000 10,000

Adjusted gross income 82,000 115,000 95,000

Standard deduction 12,550 12,550 12,550

Taxable income 69,450 102,450 82,450

Tax 11,028 18,609 13,888

Tax bracket 22% 24% 24%

Day trader making the Sec. 475(f) election

Ordinary income from other sources $95,000 $95,000 $95,000

Capital gains/losses from trading activities 0 0 0

Ordinary income/loss from trading (25,000) 30,000 30,000

Schedule C expenses 10,000 10,000 10,000

Adjusted gross income 60,000 115,000 115,000

Standard deduction 12,550 12,550 12,550

Taxable income 47,450 102,450 102,450

Tax 6,188 18,609 18,609

Tax bracket 22% 24% 24%

Tax difference with Sec. 475(f) election (4,840) 0 4,721

*The day trader’s net capital loss is subject to the $3,000 capital loss limitation.

Source: Joseph Hargadon, Irfan Safdar, Stephanie Wendling, and Eunbin Whang.

AICPA RESOURCES

The Tax Adviser and Tax Section

AICPA Tax Section members receive a subscription to The Tax Adviser digital replica online in addition to access to a tax

resource library, member-only newsletter, and four free webcasts. The Tax Section is leading tax forward with the latest

news, tools, webcasts, client support, and more. Learn more at us.aicpa.org/tax-section.

40 | Journal of Accountancy June 2022