Page 261 - JoFA_2022

P. 261

Value of split-dollar No-change partnership examinations

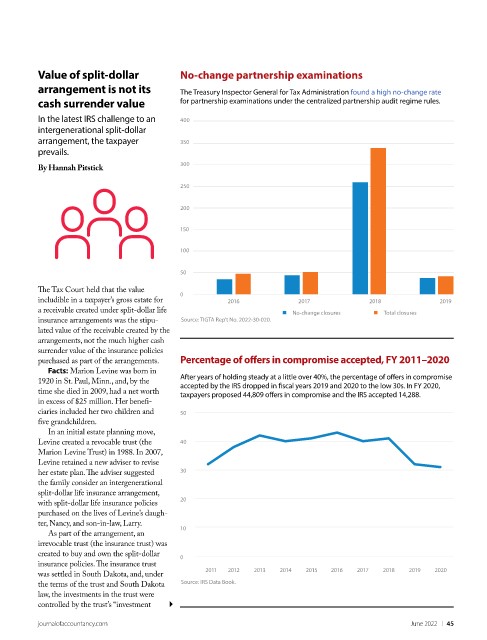

arrangement is not its The Treasury Inspector General for Tax Administration found a high no-change rate

cash surrender value for partnership examinations under the centralized partnership audit regime rules.

In the latest IRS challenge to an 400

intergenerational split-dollar

arrangement, the taxpayer 350

prevails.

300

By Hannah Pitstick

250

200

150

100

50

The Tax Court held that the value

0

includible in a taxpayer’s gross estate for 2016 2017 2018 2019

a receivable created under split-dollar life No-change closures Total closures

insurance arrangements was the stipu- Source: TIGTA Rep’t No. 2022-30-020.

lated value of the receivable created by the

arrangements, not the much higher cash

surrender value of the insurance policies

purchased as part of the arrangements. Percentage of offers in compromise accepted, FY 2011–2020

Facts: Marion Levine was born in

After years of holding steady at a little over 40%, the percentage of offers in compromise

1920 in St. Paul, Minn., and, by the

accepted by the IRS dropped in fiscal years 2019 and 2020 to the low 30s. In FY 2020,

time she died in 2009, had a net worth taxpayers proposed 44,809 offers in compromise and the IRS accepted 14,288.

in excess of $25 million. Her benefi-

ciaries included her two children and 50

five grandchildren.

In an initial estate planning move,

Levine created a revocable trust (the 40

Marion Levine Trust) in 1988. In 2007,

Levine retained a new adviser to revise

her estate plan. The adviser suggested 30

the family consider an intergenerational

split-dollar life insurance arrangement,

20

with split-dollar life insurance policies

purchased on the lives of Levine’s daugh-

ter, Nancy, and son-in-law, Larry.

10

As part of the arrangement, an

irrevocable trust (the insurance trust) was

created to buy and own the split-dollar 0

insurance policies. The insurance trust

2011 2012 2013 2014 2015 2016 2017 2018 2019 2020

was settled in South Dakota, and, under

Source: IRS Data Book.

the terms of the trust and South Dakota

law, the investments in the trust were

controlled by the trust’s “investment

journalofaccountancy.com June 2022 | 45