Page 305 - JoFA_2022

P. 305

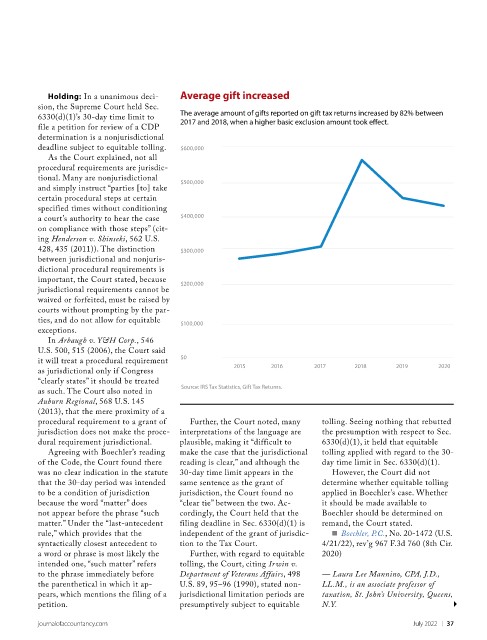

Average gift increased

Holding: In a unanimous deci-

sion, the Supreme Court held Sec.

The average amount of gifts reported on gift tax returns increased by 82% between

6330(d)(1)’s 30-day time limit to

2017 and 2018, when a higher basic exclusion amount took effect.

file a petition for review of a CDP

determination is a nonjurisdictional

deadline subject to equitable tolling. $600,000

As the Court explained, not all

procedural requirements are jurisdic-

tional. Many are nonjurisdictional

$500,000

and simply instruct “parties [to] take

certain procedural steps at certain

specified times without conditioning

$400,000

a court’s authority to hear the case

on compliance with those steps” (cit-

ing Henderson v. Shinseki, 562 U.S.

428, 435 (2011)). The distinction $300,000

between jurisdictional and nonjuris-

dictional procedural requirements is

important, the Court stated, because

$200,000

jurisdictional requirements cannot be

waived or forfeited, must be raised by

courts without prompting by the par-

ties, and do not allow for equitable $100,000

exceptions.

In Arbaugh v. Y&H Corp., 546

U.S. 500, 515 (2006), the Court said

$0

it will treat a procedural requirement

2015 2016 2017 2018 2019 2020

as jurisdictional only if Congress

“clearly states” it should be treated

Source: IRS Tax Statistics, Gift Tax Returns.

as such. The Court also noted in

Auburn Regional, 568 U.S. 145

(2013), that the mere proximity of a

procedural requirement to a grant of Further, the Court noted, many tolling. Seeing nothing that rebutted

jurisdiction does not make the proce- interpretations of the language are the presumption with respect to Sec.

dural requirement jurisdictional. plausible, making it “difficult to 6330(d)(1), it held that equitable

Agreeing with Boechler’s reading make the case that the jurisdictional tolling applied with regard to the 30-

of the Code, the Court found there reading is clear,” and although the day time limit in Sec. 6330(d)(1).

was no clear indication in the statute 30-day time limit appears in the However, the Court did not

that the 30-day period was intended same sentence as the grant of determine whether equitable tolling

to be a condition of jurisdiction jurisdiction, the Court found no applied in Boechler’s case. Whether

because the word “matter” does “clear tie” between the two. Ac- it should be made available to

not appear before the phrase “such cordingly, the Court held that the Boechler should be determined on

matter.” Under the “last-antecedent filing deadline in Sec. 6330(d)(1) is remand, the Court stated.

rule,” which provides that the independent of the grant of jurisdic- ■ Boechler, P.C., No. 20-1472 (U.S.

syntactically closest antecedent to tion to the Tax Court. 4/21/22), rev’g 967 F.3d 760 (8th Cir.

a word or phrase is most likely the Further, with regard to equitable 2020)

intended one, “such matter” refers tolling, the Court, citing Irwin v.

to the phrase immediately before Department of Veterans Affairs, 498 — Laura Lee Mannino, CPA, J.D.,

the parenthetical in which it ap- U.S. 89, 95–96 (1990), stated non- LL.M., is an associate professor of

pears, which mentions the filing of a jurisdictional limitation periods are taxation, St. John’s University, Queens,

petition. presumptively subject to equitable N.Y.

journalofaccountancy.com July 2022 | 37