Page 306 - JoFA_2022

P. 306

TAX MATTERS

testified, she was unable to pay the taxes Issues: The Bankruptcy Code

and was attempting to understand the provides that a discharge does not

reason for the deficiency’s amount. Her include an individual’s tax debt with

prepared 2008 return showed a balance respect to which a required return or

due of $23,040. In August 2011, Golden its equivalent was not filed, or that

did file the 2008 return. the debtor filed after its due date,

In April 2014, Golden and Alter including extensions, and within

filed a Chapter 13 bankruptcy petition. less than two years before filing

The IRS filed a claim for $88,516, of the bankruptcy petition (11 U.S.C.

which nearly $8,000 was identified as §523(a)(1)(B)). Among a number of

secured, nearly $50,000 as priority, and other things, the IRS claimed the

the balance of more than $30,000 shown taxpayers’ 2011 filing did not qualify

as a general unsecured claim. The couple as a return under the tests of Beard,

obtained a general discharge in February 82 T.C. 766 (1984); specifically, it did

2020 after paying more than $51,000 to not represent an honest and reason-

the IRS. In June 2020, the IRS issued able attempt to satisfy the require-

Tax debt from late return the taxpayers a notice of lien for the ments of the tax law.

is held discharged remaining taxes owed. The IRS argued that Golden and

In February 2021, Golden and Alter Alter’s return was not an honest and

A bankruptcy court holds that filed an adversary proceeding in bank- reasonable attempt to satisfy the

the taxpayers’ return was an ruptcy court against the IRS, contending requirements of the tax law because

honest and reasonable attempt that the tax debt had been discharged. their conduct with respect to the

to comply with the tax law. The IRS contended that the tax debt was return was like that of taxpayers in

nondischargeable. Both sides moved for two Ninth Circuit cases in which

By Paul Bonner

summary judgment. that court held their tax debts were

A bankruptcy court held that a

couple’s tax return filing allowed a

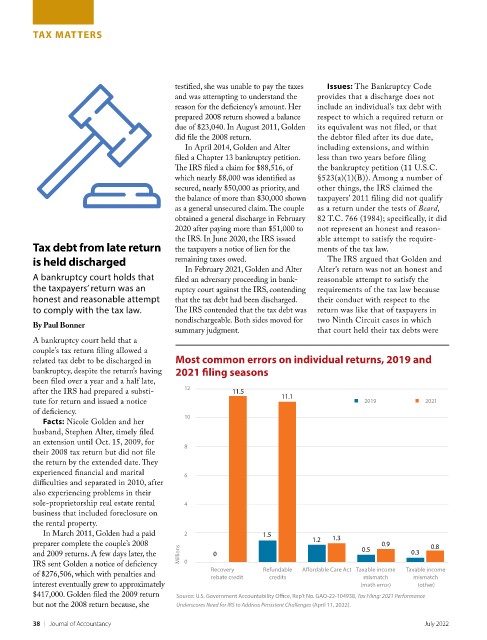

related tax debt to be discharged in Most common errors on individual returns, 2019 and

2021 filing seasons

bankruptcy, despite the return’s having

been filed over a year and a half late,

12

after the IRS had prepared a substi- 11.5

11.1

tute for return and issued a notice 2019 2021

of deficiency.

10

Facts: Nicole Golden and her

husband, Stephen Alter, timely filed

an extension until Oct. 15, 2009, for

8

their 2008 tax return but did not file

the return by the extended date. They

experienced financial and marital 6

difficulties and separated in 2010, after

also experiencing problems in their

sole-proprietorship real estate rental 4

business that included foreclosure on

the rental property.

In March 2011, Golden had a paid 2 1.5

1.2 1.3

preparer complete the couple’s 2008 0.5 0.9 0.8

and 2009 returns. A few days later, the Millions 0 0.3

IRS sent Golden a notice of deficiency 0

Recovery Refundable Affordable Care Act Taxable income Taxable income

of $276,506, which with penalties and rebate credit credits mismatch mismatch

interest eventually grew to approximately (math error) (other)

$417,000. Golden filed the 2009 return Source: U.S. Government Accountability Office, Rep’t No. GAO-22-104938, Tax Filing: 2021 Performance

but not the 2008 return because, she Underscores Need for IRS to Address Persistent Challenges (April 11, 2022).

38 | Journal of Accountancy July 2022