Page 322 - JoFA_2022

P. 322

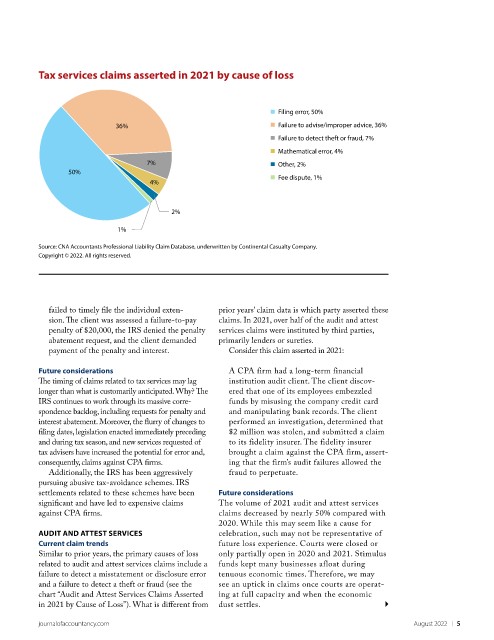

Tax services claims asserted in 2021 by cause of loss

Filing error, 50%

36% Failure to advise/improper advice, 36%

Failure to detect theft or fraud, 7%

Mathematical error, 4%

7% Other, 2%

50% Fee dispute, 1%

4%

2%

1%

Source: CNA Accountants Professional Liability Claim Database, underwritten by Continental Casualty Company.

Copyright © 2022. All rights reserved.

failed to timely file the individual exten- prior years’ claim data is which party asserted these

sion. The client was assessed a failure-to-pay claims. In 2021, over half of the audit and attest

penalty of $20,000, the IRS denied the penalty services claims were instituted by third parties,

abatement request, and the client demanded primarily lenders or sureties.

payment of the penalty and interest. Consider this claim asserted in 2021:

Future considerations A CPA firm had a long-term financial

The timing of claims related to tax services may lag institution audit client. The client discov-

longer than what is customarily anticipated. Why? The ered that one of its employees embezzled

IRS continues to work through its massive corre- funds by misusing the company credit card

spondence backlog, including requests for penalty and and manipulating bank records. The client

interest abatement. Moreover, the flurry of changes to performed an investigation, determined that

filing dates, legislation enacted immediately preceding $2 million was stolen, and submitted a claim

and during tax season, and new services requested of to its fidelity insurer. The fidelity insurer

tax advisers have increased the potential for error and, brought a claim against the CPA firm, assert-

consequently, claims against CPA firms. ing that the firm’s audit failures allowed the

Additionally, the IRS has been aggressively fraud to perpetuate.

pursuing abusive tax-avoidance schemes. IRS

settlements related to these schemes have been Future considerations

significant and have led to expensive claims The volume of 2021 audit and attest services

against CPA firms. claims decreased by nearly 50% compared with

2020. While this may seem like a cause for

AUDIT AND ATTEST SERVICES celebration, such may not be representative of

Current claim trends future loss experience. Courts were closed or

Similar to prior years, the primary causes of loss only partially open in 2020 and 2021. Stimulus

related to audit and attest services claims include a funds kept many businesses afloat during

failure to detect a misstatement or disclosure error tenuous economic times. Therefore, we may

and a failure to detect a theft or fraud (see the see an uptick in claims once courts are operat-

chart “Audit and Attest Services Claims Asserted ing at full capacity and when the economic

in 2021 by Cause of Loss”). What is different from dust settles.

journalofaccountancy.com August 2022 | 5