Page 393 - JoFA_2022

P. 393

TAX MATTERS

The rise and fall of whistleblower awards to collect the McAuliffes’ discharged

personal liabilities.

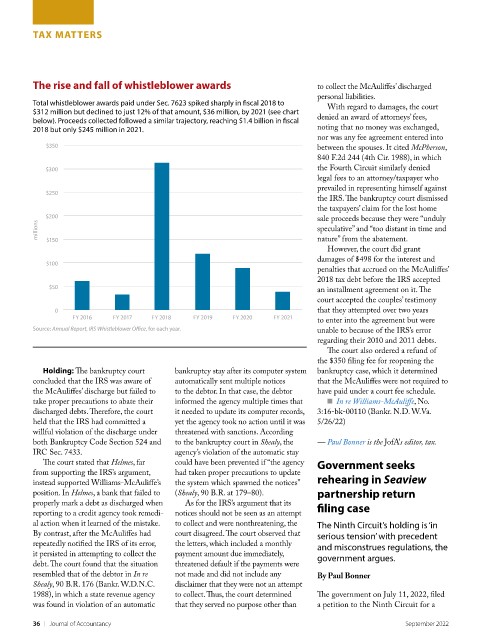

Total whistleblower awards paid under Sec. 7623 spiked sharply in fiscal 2018 to

$312 million but declined to just 12% of that amount, $36 million, by 2021 (see chart With regard to damages, the court

below). Proceeds collected followed a similar trajectory, reaching $1.4 billion in fiscal denied an award of attorneys’ fees,

2018 but only $245 million in 2021. noting that no money was exchanged,

nor was any fee agreement entered into

$350 between the spouses. It cited McPherson,

840 F.2d 244 (4th Cir. 1988), in which

$300 the Fourth Circuit similarly denied

legal fees to an attorney/taxpayer who

prevailed in representing himself against

$250

the IRS. The bankruptcy court dismissed

the taxpayers’ claim for the lost home

$200 sale proceeds because they were “unduly

millions $150 speculative” and “too distant in time and

nature” from the abatement.

However, the court did grant

damages of $498 for the interest and

$100

penalties that accrued on the McAuliffes’

2018 tax debt before the IRS accepted

$50

an installment agreement on it. The

court accepted the couples’ testimony

0 that they attempted over two years

FY 2016 FY 2017 FY 2018 FY 2019 FY 2020 FY 2021

to enter into the agreement but were

Source: Annual Report, IRS Whistleblower Office, for each year. unable to because of the IRS’s error

regarding their 2010 and 2011 debts.

The court also ordered a refund of

the $350 filing fee for reopening the

Holding: The bankruptcy court bankruptcy stay after its computer system bankruptcy case, which it determined

concluded that the IRS was aware of automatically sent multiple notices that the McAuliffes were not required to

the McAuliffes’ discharge but failed to to the debtor. In that case, the debtor have paid under a court fee schedule.

take proper precautions to abate their informed the agency multiple times that ■ In re Williams-McAuliffe, No.

discharged debts. Therefore, the court it needed to update its computer records, 3:16-bk-00110 (Bankr. N.D. W.Va.

held that the IRS had committed a yet the agency took no action until it was 5/26/22)

willful violation of the discharge under threatened with sanctions. According

both Bankruptcy Code Section 524 and to the bankruptcy court in Shealy, the — Paul Bonner is the JofA’s editor, tax.

IRC Sec. 7433. agency’s violation of the automatic stay

Government seeks

The court stated that Helmes, far could have been prevented if “the agency

from supporting the IRS’s argument, had taken proper precautions to update rehearing in Seaview

instead supported Williams-McAuliffe’s the system which spawned the notices”

partnership return

position. In Helmes, a bank that failed to (Shealy, 90 B.R. at 179–80).

properly mark a debt as discharged when As for the IRS’s argument that its filing case

reporting to a credit agency took remedi- notices should not be seen as an attempt

al action when it learned of the mistake. to collect and were nonthreatening, the The Ninth Circuit’s holding is ‘in

By contrast, after the McAuliffes had court disagreed. The court observed that serious tension’ with precedent

repeatedly notified the IRS of its error, the letters, which included a monthly and misconstrues regulations, the

it persisted in attempting to collect the payment amount due immediately, government argues.

debt. The court found that the situation threatened default if the payments were

resembled that of the debtor in In re not made and did not include any By Paul Bonner

Shealy, 90 B.R. 176 (Bankr. W.D.N.C. disclaimer that they were not an attempt

1988), in which a state revenue agency to collect. Thus, the court determined The government on July 11, 2022, filed

was found in violation of an automatic that they served no purpose other than a petition to the Ninth Circuit for a

36 | Journal of Accountancy September 2022