Page 43 - JoFA_2022

P. 43

IRS addresses taxpayer IRS innocent spouse appeals received, closed,

reliance on FAQs and pending

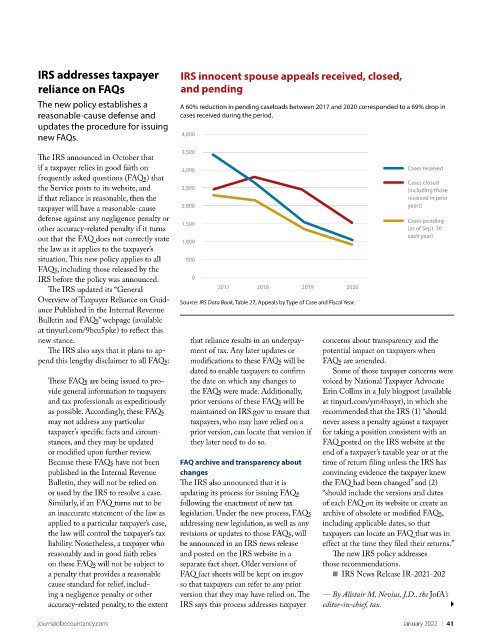

The new policy establishes a A 60% reduction in pending caseloads between 2017 and 2020 corresponded to a 69% drop in

reasonable-cause defense and cases received during the period.

updates the procedure for issuing

new FAQs. 4,000

3,500

The IRS announced in October that

if a taxpayer relies in good faith on 3,000 Cases received

frequently asked questions (FAQs) that

Cases closed

the Service posts to its website, and 2,500 (including those

if that reliance is reasonable, then the received in prior

2,000 years)

taxpayer will have a reasonable-cause

defense against any negligence penalty or Cases pending

1,500

other accuracy-related penalty if it turns (as of Sept. 30

each year)

out that the FAQ does not correctly state 1,000

the law as it applies to the taxpayer’s

situation. This new policy applies to all 500

FAQs, including those released by the

IRS before the policy was announced. 0

2017 2018 2019 2020

The IRS updated its “General

Overview of Taxpayer Reliance on Guid- Source: IRS Data Book, Table 27, Appeals by Type of Case and Fiscal Year.

ance Published in the Internal Revenue

Bulletin and FAQs” webpage (available

at tinyurl.com/9bcu5pke) to reflect this

new stance. that reliance results in an underpay- concerns about transparency and the

The IRS also says that it plans to ap- ment of tax. Any later updates or potential impact on taxpayers when

pend this lengthy disclaimer to all FAQs: modifications to these FAQs will be FAQs are amended.

dated to enable taxpayers to confirm Some of those taxpayer concerns were

These FAQs are being issued to pro- the date on which any changes to voiced by National Taxpayer Advocate

vide general information to taxpayers the FAQs were made. Additionally, Erin Collins in a July blogpost (available

and tax professionals as expeditiously prior versions of these FAQs will be at tinyurl.com/ym4hxsyr), in which she

as possible. Accordingly, these FAQs maintained on IRS.gov to ensure that recommended that the IRS (1) “should

may not address any particular taxpayers, who may have relied on a never assess a penalty against a taxpayer

taxpayer’s specific facts and circum- prior version, can locate that version if for taking a position consistent with an

stances, and they may be updated they later need to do so. FAQ posted on the IRS website at the

or modified upon further review. end of a taxpayer’s taxable year or at the

Because these FAQs have not been FAQ archive and transparency about time of return filing unless the IRS has

published in the Internal Revenue changes convincing evidence the taxpayer knew

Bulletin, they will not be relied on The IRS also announced that it is the FAQ had been changed” and (2)

or used by the IRS to resolve a case. updating its process for issuing FAQs “should include the versions and dates

Similarly, if an FAQ turns out to be following the enactment of new tax of each FAQ on its website or create an

an inaccurate statement of the law as legislation. Under the new process, FAQs archive of obsolete or modified FAQs,

applied to a particular taxpayer’s case, addressing new legislation, as well as any including applicable dates, so that

the law will control the taxpayer’s tax revisions or updates to those FAQs, will taxpayers can locate an FAQ that was in

liability. Nonetheless, a taxpayer who be announced in an IRS news release effect at the time they filed their returns.”

reasonably and in good faith relies and posted on the IRS website in a The new IRS policy addresses

on these FAQs will not be subject to separate fact sheet. Older versions of those recommendations.

a penalty that provides a reasonable FAQ fact sheets will be kept on irs.gov ■ IRS News Release IR-2021-202

cause standard for relief, includ- so that taxpayers can refer to any prior

ing a negligence penalty or other version that they may have relied on. The — By Alistair M. Nevius, J.D., the JofA’s

accuracy-related penalty, to the extent IRS says this process addresses taxpayer editor-in-chief, tax.

journalofaccountancy.com January 2022 | 41