Page 430 - JoFA_2022

P. 430

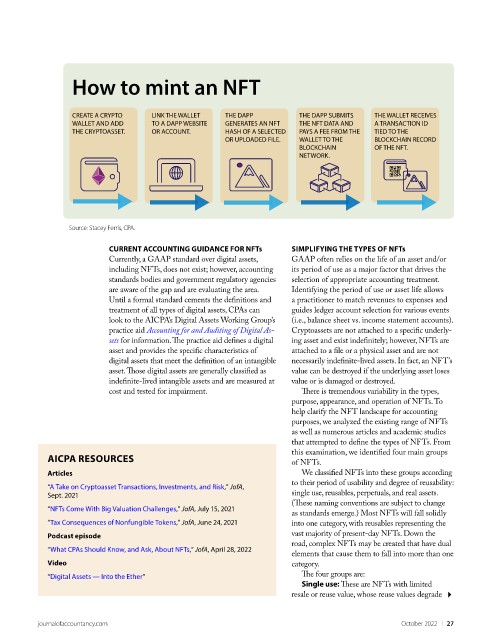

How to mint an NFT

CREATE A CRYPTO LINK THE WALLET THE DAPP THE DAPP SUBMITS THE WALLET RECEIVES

WALLET AND ADD TO A DAPP WEBSITE GENERATES AN NFT THE NFT DATA AND A TRANSACTION ID

THE CRYPTOASSET. OR ACCOUNT. HASH OF A SELECTED PAYS A FEE FROM THE TIED TO THE

OR UPLOADED FILE. WALLET TO THE BLOCKCHAIN RECORD

BLOCKCHAIN OF THE NFT.

NETWORK.

Source: Stacey Ferris, CPA.

CURRENT ACCOUNTING GUIDANCE FOR NFTs SIMPLIFYING THE TYPES OF NFTs

Currently, a GAAP standard over digital assets, GAAP often relies on the life of an asset and/or

including NFTs, does not exist; however, accounting its period of use as a major factor that drives the

standards bodies and government regulatory agencies selection of appropriate accounting treatment.

are aware of the gap and are evaluating the area. Identifying the period of use or asset life allows

Until a formal standard cements the definitions and a practitioner to match revenues to expenses and

treatment of all types of digital assets, CPAs can guides ledger account selection for various events

look to the AICPA’s Digital Assets Working Group’s (i.e., balance sheet vs. income statement accounts).

practice aid Accounting for and Auditing of Digital As- Cryptoassets are not attached to a specific underly-

sets for information. The practice aid defines a digital ing asset and exist indefinitely; however, NFTs are

asset and provides the specific characteristics of attached to a file or a physical asset and are not

digital assets that meet the definition of an intangible necessarily indefinite-lived assets. In fact, an NFT’s

asset. Those digital assets are generally classified as value can be destroyed if the underlying asset loses

indefinite-lived intangible assets and are measured at value or is damaged or destroyed.

cost and tested for impairment. There is tremendous variability in the types,

purpose, appearance, and operation of NFTs. To

help clarify the NFT landscape for accounting

purposes, we analyzed the existing range of NFTs

as well as numerous articles and academic studies

that attempted to define the types of NFTs. From

AICPA RESOURCES this examination, we identified four main groups

of NFTs.

Articles We classified NFTs into these groups according

“A Take on Cryptoasset Transactions, Investments, and Risk,” JofA, to their period of usability and degree of reusability:

Sept. 2021 single use, reusables, perpetuals, and real assets.

(These naming conventions are subject to change

“NFTs Come With Big Valuation Challenges,” JofA, July 15, 2021

as standards emerge.) Most NFTs will fall solidly

“Tax Consequences of Nonfungible Tokens,” JofA, June 24, 2021 into one category, with reusables representing the

Podcast episode vast majority of present-day NFTs. Down the

road, complex NFTs may be created that have dual

“What CPAs Should Know, and Ask, About NFTs,” JofA, April 28, 2022

elements that cause them to fall into more than one

Video category.

“Digital Assets — Into the Ether” The four groups are:

Single use: These are NFTs with limited

resale or reuse value, whose reuse values degrade

journalofaccountancy.com October 2022 | 27