Page 434 - JoFA_2022

P. 434

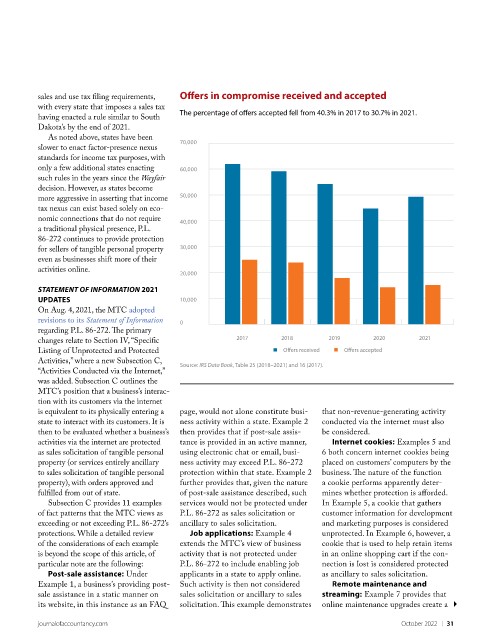

sales and use tax filing requirements, Offers in compromise received and accepted

with every state that imposes a sales tax

The percentage of offers accepted fell from 40.3% in 2017 to 30.7% in 2021.

having enacted a rule similar to South

Dakota’s by the end of 2021.

As noted above, states have been

70,000

slower to enact factor-presence nexus

standards for income tax purposes, with

only a few additional states enacting 60,000

such rules in the years since the Wayfair

decision. However, as states become

50,000

more aggressive in asserting that income

tax nexus can exist based solely on eco-

nomic connections that do not require 40,000

a traditional physical presence, P.L.

86-272 continues to provide protection

for sellers of tangible personal property 30,000

even as businesses shift more of their

activities online.

20,000

STATEMENT OF INFORMATION 2021

UPDATES 10,000

On Aug. 4, 2021, the MTC adopted

revisions to its Statement of Information 0

regarding P.L. 86-272. The primary

2017 2018 2019 2020 2021

changes relate to Section IV, “Specific

Listing of Unprotected and Protected Offers received Offers accepted

Activities,” where a new Subsection C,

Source: IRS Data Book, Table 25 (2018–2021) and 16 (2017).

“Activities Conducted via the Internet,”

was added. Subsection C outlines the

MTC’s position that a business’s interac-

tion with its customers via the internet

is equivalent to its physically entering a page, would not alone constitute busi- that non-revenue-generating activity

state to interact with its customers. It is ness activity within a state. Example 2 conducted via the internet must also

then to be evaluated whether a business’s then provides that if post-sale assis- be considered.

activities via the internet are protected tance is provided in an active manner, Internet cookies: Examples 5 and

as sales solicitation of tangible personal using electronic chat or email, busi- 6 both concern internet cookies being

property (or services entirely ancillary ness activity may exceed P.L. 86-272 placed on customers’ computers by the

to sales solicitation of tangible personal protection within that state. Example 2 business. The nature of the function

property), with orders approved and further provides that, given the nature a cookie performs apparently deter-

fulfilled from out of state. of post-sale assistance described, such mines whether protection is afforded.

Subsection C provides 11 examples services would not be protected under In Example 5, a cookie that gathers

of fact patterns that the MTC views as P.L. 86-272 as sales solicitation or customer information for development

exceeding or not exceeding P.L. 86-272’s ancillary to sales solicitation. and marketing purposes is considered

protections. While a detailed review Job applications: Example 4 unprotected. In Example 6, however, a

of the considerations of each example extends the MTC’s view of business cookie that is used to help retain items

is beyond the scope of this article, of activity that is not protected under in an online shopping cart if the con-

particular note are the following: P.L. 86-272 to include enabling job nection is lost is considered protected

Post-sale assistance: Under applicants in a state to apply online. as ancillary to sales solicitation.

Example 1, a business’s providing post- Such activity is then not considered Remote maintenance and

sale assistance in a static manner on sales solicitation or ancillary to sales streaming: Example 7 provides that

its website, in this instance as an FAQ solicitation. This example demonstrates online maintenance upgrades create a

journalofaccountancy.com October 2022 | 31