Page 70 - JoFA_2022

P. 70

FIRM PRACTICE MANAGEMENT

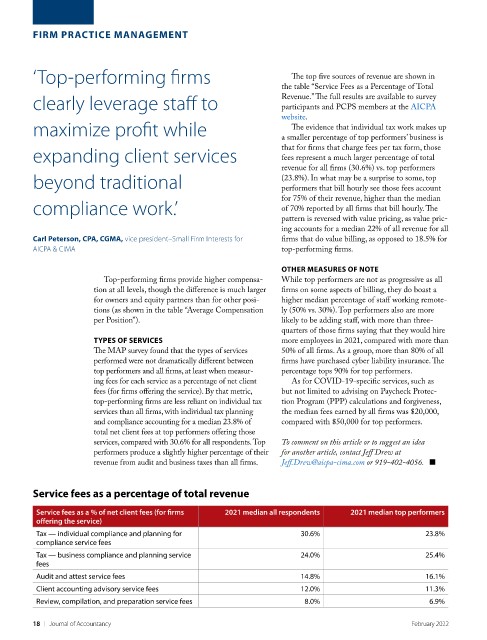

‘Top-performing firms The top five sources of revenue are shown in

the table “Service Fees as a Percentage of Total

clearly leverage staff to Revenue.” The full results are available to survey

participants and PCPS members at the AICPA

website.

maximize profit while The evidence that individual tax work makes up

a smaller percentage of top performers’ business is

expanding client services that for firms that charge fees per tax form, those

fees represent a much larger percentage of total

revenue for all firms (30.6%) vs. top performers

beyond traditional (23.8%). In what may be a surprise to some, top

performers that bill hourly see those fees account

compliance work.’ for 75% of their revenue, higher than the median

of 70% reported by all firms that bill hourly. The

pattern is reversed with value pricing, as value pric-

ing accounts for a median 22% of all revenue for all

Carl Peterson, CPA, CGMA, vice president–Small Firm Interests for firms that do value billing, as opposed to 18.5% for

AICPA & CIMA top-performing firms.

OTHER MEASURES OF NOTE

Top-performing firms provide higher compensa- While top performers are not as progressive as all

tion at all levels, though the difference is much larger firms on some aspects of billing, they do boast a

for owners and equity partners than for other posi- higher median percentage of staff working remote-

tions (as shown in the table “Average Compensation ly (50% vs. 30%). Top performers also are more

per Position”). likely to be adding staff, with more than three-

quarters of those firms saying that they would hire

TYPES OF SERVICES more employees in 2021, compared with more than

The MAP survey found that the types of services 50% of all firms. As a group, more than 80% of all

performed were not dramatically different between firms have purchased cyber liability insurance. The

top performers and all firms, at least when measur- percentage tops 90% for top performers.

ing fees for each service as a percentage of net client As for COVID-19-specific services, such as

fees (for firms offering the service). By that metric, but not limited to advising on Paycheck Protec-

top-performing firms are less reliant on individual tax tion Program (PPP) calculations and forgiveness,

services than all firms, with individual tax planning the median fees earned by all firms was $20,000,

and compliance accounting for a median 23.8% of compared with $50,000 for top performers.

total net client fees at top performers offering those

services, compared with 30.6% for all respondents. Top To comment on this article or to suggest an idea

performers produce a slightly higher percentage of their for another article, contact Jeff Drew at

revenue from audit and business taxes than all firms. Jeff.Drew@aicpa-cima.com or 919-402-4056. ■

Service fees as a percentage of total revenue

Service fees as a % of net client fees (for firms 2021 median all respondents 2021 median top performers

offering the service)

Tax — individual compliance and planning for 30.6% 23.8%

compliance service fees

Tax — business compliance and planning service 24.0% 25.4%

fees

Audit and attest service fees 14.8% 16.1%

Client accounting advisory service fees 12.0% 11.3%

Review, compilation, and preparation service fees 8.0% 6.9%

18 | Journal of Accountancy February 2022