Page 260 - ACFE Fraud Reports 2009_2020

P. 260

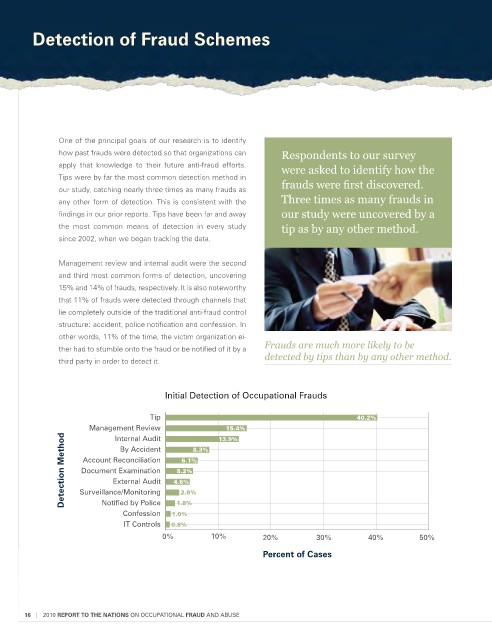

Detection of Fraud schemes

One of the principal goals of our research is to identify

how past frauds were detected so that organizations can Respondents to our survey

apply that knowledge to their future anti-fraud efforts. were asked to identify how the

Tips were by far the most common detection method in

our study, catching nearly three times as many frauds as frauds were first discovered.

any other form of detection. This is consistent with the Three times as many frauds in

findings in our prior reports. Tips have been far and away our study were uncovered by a

the most common means of detection in every study tip as by any other method.

since 2002, when we began tracking the data.

Management review and internal audit were the second

and third most common forms of detection, uncovering

15% and 14% of frauds, respectively. It is also noteworthy

that 11% of frauds were detected through channels that

lie completely outside of the traditional anti-fraud control

structure: accident, police notification and confession. In

other words, 11% of the time, the victim organization ei-

ther had to stumble onto the fraud or be notified of it by a Frauds are much more likely to be

third party in order to detect it. detected by tips than by any other method.

Initial detection of Occupational Frauds

Tip 40.2%

Management Review 13.9%

15.4%

Detection Method Surveillance/Monitoring 4.6% 8.3%

Internal Audit

By Accident

Account Reconciliation

6.1%

Document Examination

5.2%

External Audit

2.6%

Notified by Police

1.8%

Confession 1.0%

IT Controls 0.8%

0% 10% 20% 30% 40% 50%

Percent of Cases

16 | 2010 RepoRt to the NAtioNs ON OccuPATIONAl FRAUD ANd AbuSE