Page 263 - ACFE Fraud Reports 2009_2020

P. 263

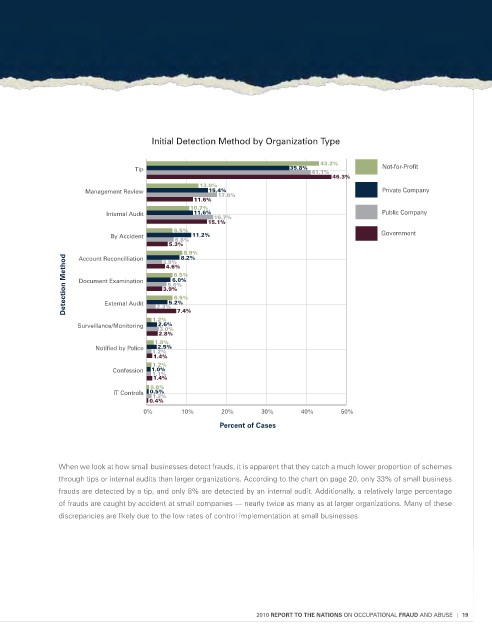

Initial detection Method by Organization Type

43.2%

Tip 35.8% Not-for-Profit

41.1%

46.3%

13.0%

Management Review 15.4% Private Company

17.6%

11.6%

10.7%

Internal Audit 11.6% 16.7% Public Company

15.1%

6.5% Government

By Accident 6.8% 11.2%

5.3%

8.9%

8.2%

Detection Method Document Examination 3.9% 6.5%

Account Reconcilliation

3.9%

4.6%

6.0%

5.0%

6.5%

5.2%

External Audit

2.3%

1.2% 7.4%

Surveillance/Monitoring 2.6%

3.0%

2.8%

1.8%

Notified by Police 2.5%

1.2%

1.4%

1.2%

Confession 1.0%

1.1%

1.4%

0.6%

IT Controls 0.5%

1.2%

0.4%

0% 10% 20% 30% 40% 50%

Percent of Cases

When we look at how small businesses detect frauds, it is apparent that they catch a much lower proportion of schemes

through tips or internal audits than larger organizations. According to the chart on page 20, only 33% of small business

frauds are detected by a tip, and only 8% are detected by an internal audit. Additionally, a relatively large percentage

of frauds are caught by accident at small companies — nearly twice as many as at larger organizations. Many of these

discrepancies are likely due to the low rates of control implementation at small businesses.

2010 RepoRt to the NAtioNs ON OccuPATIONAl FRAUD ANd AbuSE | 19