Page 264 - ACFE Fraud Reports 2009_2020

P. 264

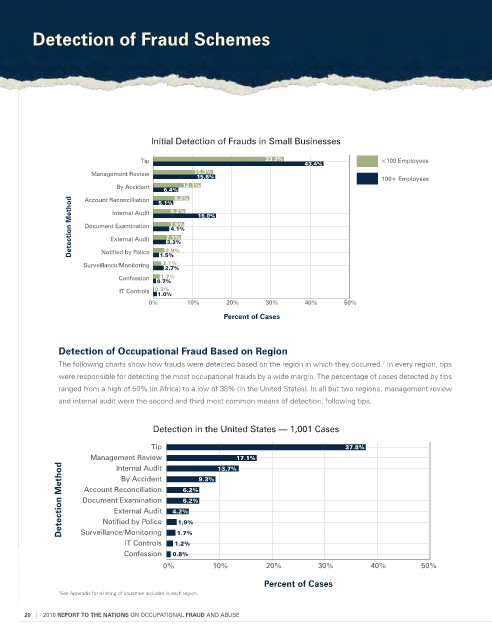

Detection of Fraud schemes

Initial detection of Frauds in Small businesses

Tip 33.3% <100 Employees

43.4%

Management Review 15.3%

15.8% 100+ Employees

By Accident 12.1%

6.4% 9.2%

Account Reconcilliation

Detection Method Document Examination 7.1% 16.0%

5.1%

8.2%

Internal Audit

7.9%

4.1%

External Audit

3.3%

2.9%

Notified by Police

2.1%

Surveillance/Monitoring 1.5%

2.7%

1.7%

Confession 0.7%

IT Controls 0.2%

1.0%

0% 10% 20% 30% 40% 50%

Percent of Cases

Detection of occupational Fraud Based on Region

The following charts show how frauds were detected based on the region in which they occurred. In every region, tips

7

were responsible for detecting the most occupational frauds by a wide margin. The percentage of cases detected by tips

ranged from a high of 50% (in Africa) to a low of 38% (in the United States). In all but two regions, management review

and internal audit were the second and third most common means of detection, following tips.

detection in the united States — 1,001 cases

Tip 37.8%

Management Review 13.7% 17.1%

Detection Method Document Examination 4.2% 9.3%

Internal Audit

By Accident

Account Reconciliation

6.2%

6.2%

External Audit

Notified by Police

1.9%

Surveillance/Monitoring

1.7%

IT Controls 1.2%

Confession 0.8%

0% 10% 20% 30% 40% 50%

Percent of Cases

7 See Appendix for a listing of countries included in each region.

20 | 2010 RepoRt to the NAtioNs ON OccuPATIONAl FRAUD ANd AbuSE